Quick Answer

Buy if you plan to stay in one place for at least 3 to 5 years, have stable income, and can afford a down payment plus ongoing costs. Rent if you need flexibility, aren’t sure where you want to live, or aren’t financially ready for homeownership. There’s no universally right answer. It depends on your situation.

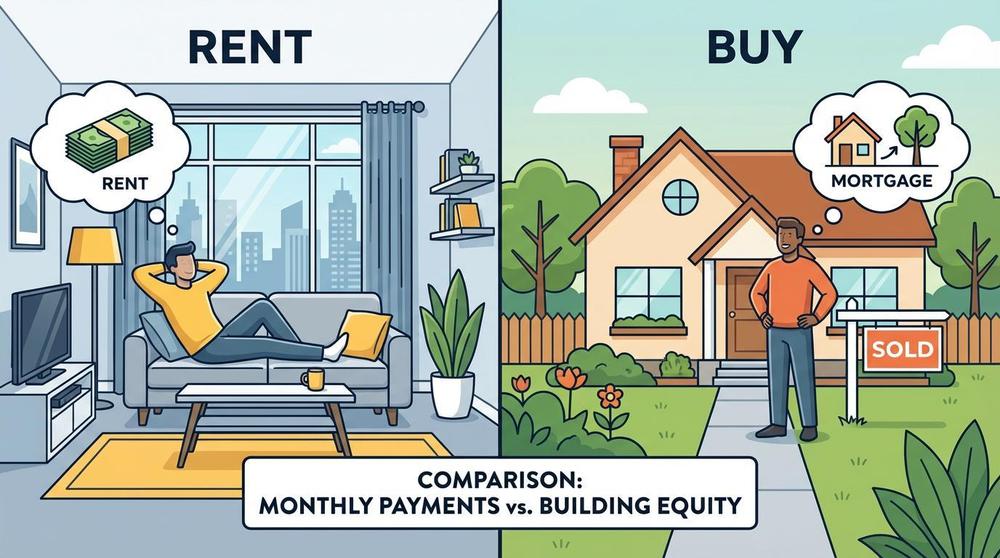

The Case for Buying

Buying a home is one of the most common ways people build long-term wealth. But it only works if the timing and finances are right.

You Build Equity

Every payment puts money toward owning your home outright. Over time, your equity grows, especially if home values increase in your area. When you sell, that equity is yours.

Your Payment Can Be Predictable

With a fixed-rate loan, your principal and interest payment stays the same for the life of the loan. Rent, on the other hand, almost always goes up over time.

Tax Benefits

Homeowners can deduct property taxes and loan interest in many situations. These deductions can reduce your overall tax burden, though you should talk to a tax professional about your specific case.

It’s Yours

Want to paint the walls, rip out carpet, or build a deck? Go for it. When you own, you make the rules. No landlord approval needed.

The Case for Renting

Renting isn’t throwing money away. It’s paying for flexibility and lower risk.

Flexibility

Renting lets you move when your lease is up. If your job changes, your relationship changes, or you just want a new neighborhood, you’re not locked in. Selling a house takes time and money.

Lower Upfront Costs

A security deposit and first month’s rent is a lot less than a down payment, closing costs, and moving into a home you now have to maintain. Renting keeps your cash liquid.

No Maintenance Costs

When the furnace breaks or the roof leaks, the landlord pays. When you own a home, that’s your problem and your checkbook.

Less Financial Risk

If home values drop, a homeowner loses equity. A renter isn’t affected. If you’re not sure about a market or your long-term plans, renting reduces risk.

Key Questions to Ask Yourself

How Long Will You Stay?

Buying makes more sense if you plan to stay at least 3 to 5 years. The upfront costs of buying (closing costs, moving, repairs) take time to recover. If you’re likely to move in a year or two, renting is usually smarter.

Can You Afford the Full Cost of Owning?

Homeownership costs more than the payment. Add in property taxes, insurance, maintenance, repairs, and possibly HOA fees. A good rule of thumb: expect to spend 1% to 2% of your home’s value on maintenance each year.

Is Your Income Stable?

Buying a home requires a steady income to cover payments. If your job situation is uncertain or you’re between careers, renting gives you a safer financial cushion.

Do You Have an Emergency Fund?

Homeowners need cash reserves for unexpected repairs. A broken water heater, a roof leak, or a flooded basement can cost thousands. If you don’t have at least 3 to 6 months of expenses saved, consider building that up before buying.

What Does Your Local Market Look Like?

In some areas, buying is cheaper than renting. In others, it’s the opposite. Compare the cost of renting a similar home to what you’d pay monthly as an owner. Your real estate agent can help with this analysis.

The Break-Even Point

There’s a financial tipping point where buying becomes cheaper than renting. It depends on home prices, rent prices, taxes, and how long you stay.

A Simple Way to Think About It

If your total monthly cost of owning (payment, taxes, insurance, maintenance) is close to what you’d pay in rent, and you plan to stay 5+ years, buying likely wins in the long run because of equity.

If owning costs significantly more per month, or you’ll move within 2–3 years, renting probably saves you money.

Common Myths

”Renting Is Throwing Money Away”

No, it’s not. Renting provides shelter, flexibility, and freedom from maintenance costs. Buying also has costs that don’t build equity, like taxes, insurance, and interest.

”You Should Always Buy as Soon as Possible”

Not if you can’t afford it or aren’t staying long. Buying before you’re ready can lead to financial stress or losses if the market dips.

”Real Estate Always Goes Up”

Usually, yes, over the long term. But not always. And not everywhere. Short-term dips happen. If you need to sell during a downturn, you could lose money.

Frequently Asked Questions

At what point does buying make more sense than renting?

Buying generally makes more sense when you plan to stay at least 3 to 5 years, have a stable income, and can afford a down payment plus reserves. The longer you stay, the more buying pays off.

Is it smarter to rent and invest the difference?

It can be, depending on your investment returns and local real estate market. If you’re disciplined about investing what you’d spend on a down payment and maintenance, renting-and-investing can work. Most people aren’t that disciplined, which is why buying often wins as a “forced savings” tool.

Should I buy just because interest rates are low?

Low rates help affordability, but they shouldn’t be the only reason you buy. If you’re not ready financially or personally, waiting is fine. Rates change, but a bad buying decision doesn’t fix itself.

Bottom Line

Renting and buying are both valid choices. The right one depends on your finances, your timeline, and what matters most to you. Don’t let pressure from others push you into buying before you’re ready, and don’t assume renting is a waste. Run the numbers, consider your plans, and make the choice that fits your life.