Quick Answer

You’re financially ready to buy a house when you have stable income, a down payment saved, low debt, a good credit score, and an emergency fund. If your monthly housing cost would be 28% or less of your gross income, you’re in a strong position.

The 5-Point Readiness Checklist

Use these five checks to see if you’re ready.

1. Stable Income

You need steady, reliable income. Lenders want to see at least two years of consistent employment or income history.

If you recently changed jobs, that’s okay - as long as you stayed in the same field. Gaps or major changes can delay approval.

2. Down Payment Saved

For a conventional loan, you’ll need 5–20% of the home price. FHA loans allow as little as 3.5%.

On a $200,000 home:

- 5% down = $10,000

- 10% down = $20,000

- 20% down = $40,000 (avoids PMI)

The more you put down, the lower your monthly payment.

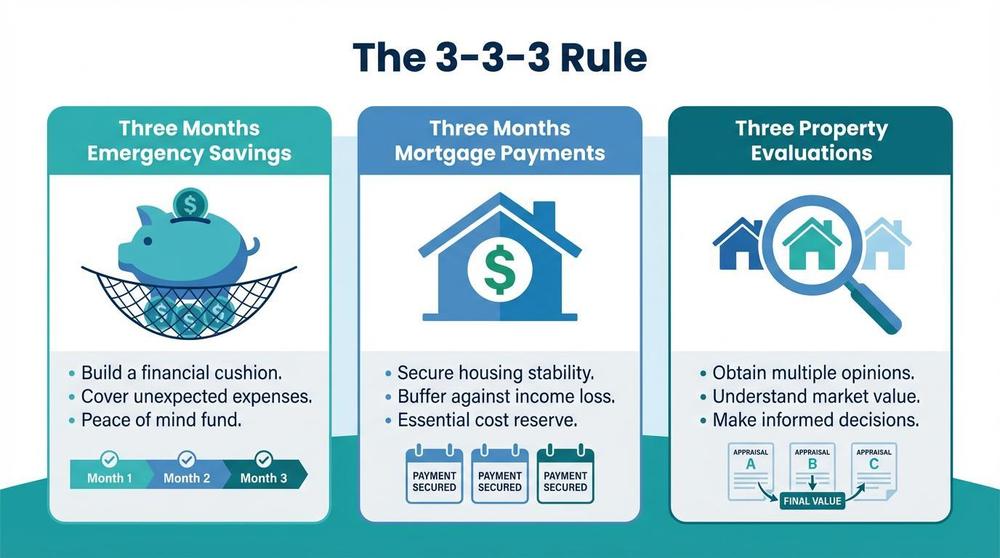

3. Emergency Fund

Keep 3–6 months of living expenses saved - separate from your down payment. This covers job loss, medical bills, or home repairs.

The 3-3-3 rule says to have three months of emergency savings plus three months of mortgage payments saved.

4. Low Debt-to-Income Ratio

Your debt-to-income ratio (DTI) is your total monthly debt divided by your gross monthly income. Lenders want this at 43% or less. Below 36% is even better.

Example:

- Gross income: $5,000/month

- Total debt payments: $1,500/month

- DTI: 30% ✓

Include car payments, student loans, credit cards, and the future mortgage payment.

5. Credit Score of 620+

Most conventional loans need a 620 credit score. FHA loans may go as low as 580. The higher your score, the better your interest rate.

Check your credit report for errors. Paying down credit cards can quickly boost your score.

The 28/36 Rule

This is one of the simplest ways to check if you can afford a home.

What It Means

- 28% – Your monthly housing cost should be 28% or less of your gross income.

- 36% – Your total monthly debt (housing + all other debt) should be 36% or less.

Example

- Gross income: $6,000/month

- 28% of $6,000 = $1,680 max housing payment

- 36% of $6,000 = $2,160 max total debt

If a home’s total monthly cost (mortgage, taxes, insurance) fits under $1,680, you’re in a good range.

Signs You’re NOT Ready Yet

Be honest with yourself. If any of these apply, wait a bit longer.

- You have no savings beyond the down payment.

- You’re carrying high-interest credit card debt.

- Your income is unstable or brand new.

- You’d have to borrow the down payment.

- The monthly payment would be more than 30% of your income.

Waiting isn’t failure. It’s smart planning.

Signs You ARE Ready

- You’ve saved a down payment and an emergency fund.

- Your debt is low or paid off.

- Your income is steady and documented.

- Your credit score is 620 or higher.

- You can afford the monthly payment without stress.

- You plan to stay in the area for at least 3–5 years.

If most of these fit, you’re likely ready.

What to Do If You’re Almost Ready

Pay Down Debt First

Focus on credit cards and high-interest loans. Every dollar of debt you remove improves your DTI and buying power.

Boost Your Credit Score

Pay bills on time. Lower your credit card balances to under 30% of your limit. Don’t open new accounts.

Keep Saving

Even small monthly deposits add up. Set up automatic transfers to a savings account dedicated to your home fund.

Frequently Asked Questions

How much money should I have saved before buying a house?

At minimum, save enough for your down payment (3.5–20%), closing costs (2–5% of the home price), and 3–6 months of living expenses as an emergency fund. For a $200,000 home, that could be $20,000–$55,000 total.

What credit score do I need to buy a house?

Most conventional loans need a 620 score. FHA loans may accept 580 with a 3.5% down payment. A higher score gets you a lower interest rate, which saves thousands over the life of the loan.

Can I buy a house if I have student loans?

Yes. Student loans affect your debt-to-income ratio, but they don’t disqualify you. If your DTI is under 43% with the student loan payments included, you can still qualify.

Bottom Line

You’re ready to buy when the numbers work and you have a safety net. Use the checklist above. If you check most of the boxes, start talking to a lender.

Your next step: Get pre-approved. It’s free, it doesn’t hurt your credit much, and it tells you exactly what you can afford.