Quick Answer:

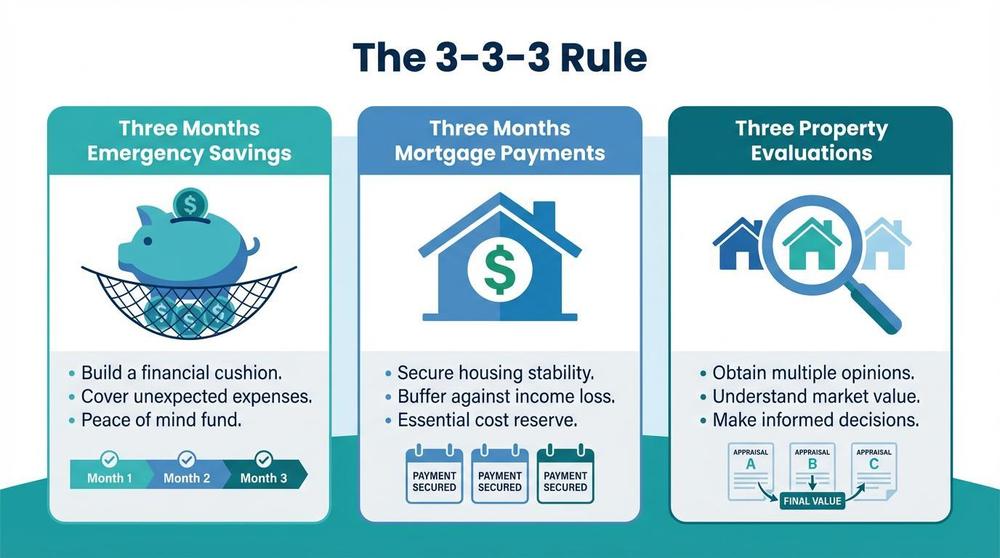

The 3-3-3 rule in real estate is a simple checklist to see if you’re ready to buy. You need: (1) three months of emergency savings, (2) three months of mortgage payments saved, and (3) three property evaluations before you make an offer. It helps you avoid buying a home you can’t afford and keeps you from rushing into a bad deal.

What Is the 3-3-3 Rule?

The 3-3-3 rule is a financial guide for home buyers and real estate investors. It tells you what to have in place before you buy a property. Each “3” stands for something you need to do or have saved.

The three parts are:

- Three months of emergency savings

- Three months of mortgage payments saved

- Three property evaluations before you buy

This rule helps protect you from buying too soon or spending more than you can handle. It works for first-time buyers, investors, and anyone buying land or a home.

The Three Parts Explained

1. Three Months of Emergency Savings

You should have at least three months of living expenses saved before you buy. This covers things like food, bills, and basic costs if something goes wrong.

Why it matters:

- Covers surprise repairs (like a broken furnace)

- Helps if you lose your job or income drops

- Keeps you from using credit cards or loans when things get tight

Add up your monthly bills. Multiply by three. That’s your target.

2. Three Months of Mortgage Payments Saved

On top of emergency savings, keep three months of mortgage payments in the bank. This is a safety net just for your housing costs.

Why it matters:

- Covers your mortgage if income slows down

- Helps with rental vacancies if you’re an investor

- Gives you time to fix money problems without missing payments

This is separate from your emergency fund. Both are important.

3. Three Property Evaluations Before Buying

Compare at least three different properties before you choose one. Look at price, location, condition, and what you get for the money.

Why it matters:

- Helps you see what’s a fair price

- Shows you what you can get in your budget

- Stops you from overpaying or buying on impulse

You don’t have to buy the third one. The goal is to learn the market before you decide.

Who Should Use the 3-3-3 Rule?

First-Time Home Buyers

Buying your first home comes with new costs. Repairs, taxes, and upkeep add up. The 3-3-3 rule helps you stay ahead of surprises.

Real Estate Investors

If you buy rental properties, you need cash for vacancies and repairs. Three months of mortgage payments gives you a buffer when a unit sits empty.

Land Buyers

Land often needs surveys, grading, or utilities. Extra savings help you cover these costs without going into debt.

Common Mistakes to Avoid

- Skipping savings – Don’t buy with almost no money left. You’ll struggle if something breaks.

- Only looking at one property – You might overpay. Compare at least three.

- Ignoring taxes and insurance – Your real cost is more than the mortgage. Plan for it.

- Rushing – Take time to save and compare. A few months of prep can save you years of stress.

Frequently Asked Questions

What is the 3-3-3 rule in real estate?

The 3-3-3 rule means: three months of emergency savings, three months of mortgage payments saved, and three property evaluations before you buy. It’s a readiness checklist for buyers and investors.

Who created the 3-3-3 rule?

The rule comes from real estate and financial experts. There’s no single source. It’s a common guideline used by agents and advisors.

Does the 3-3-3 rule apply to rental properties?

Yes. Some people use a slightly different version for rentals: three months of mortgage reserves, three months to find a tenant, and three years to judge how the property performs. The idea is the same—don’t overextend yourself.

What if I don’t have three months of savings yet?

Use the rule as a goal. Save what you can and compare properties while you build your fund. Buying when you’re not ready can lead to foreclosure or stress.

Is the 3-3-3 rule required by lenders?

No. Lenders have their own rules (like down payment and debt-to-income limits). The 3-3-3 rule is extra guidance to help you stay financially healthy after you buy.

How do I compare three properties?

Visit them, check prices, and note what each offers. Look at location, size, condition, and total cost. Write down pros and cons. This helps you see which one is the best value.

Conclusion: Your Next Steps

The 3-3-3 rule keeps you from buying a home before you’re ready. It’s simple, but it works.

What to do next:

- Calculate your savings – Add up three months of living expenses and three months of mortgage payments. See how close you are.

- Set a savings goal – If you’re short, create a plan to save each month.

- Compare properties – Look at at least three homes or properties before you make an offer.

- Talk to an agent – A local agent can help you understand prices and what to expect in your area. Also read whether to wait for lower mortgage rates.

Follow the 3-3-3 rule and you’ll be better prepared to buy a home you can afford and keep.